Week 21: What now, Big Oil?

In this issue: ▸ Big Oil’s week from Hell ▸ What about Saudi Arabia, Russia, Qatar, Venezuela etc? ▸ Run, hippo, run! ▸ Are we ready for a just transition? ▸ And much more...

Dear all,

I hope everyone is well and ready for a new edition of ‘ESG on a Sunday’!

Big Oil’s week from Hell

This past week has been rather turbulent in the ESG space. Oil and gas companies being ordered by courts to do more to reduce emissions. Other oil and gas companies experiencing shareholder mutiny. And reports on how hollow “net-zero” targets are for oil and gas companies.

Here you can read about how shareholders in Exxon and Chevron voted for measures that could force the companies to take more responsibility for its emissions.

And here’s the verdict (in English) from a Dutch court against Shell. A verdict that is basically forcing the company to slash its pollution.

What about Saudi Arabia, Russia, Qatar, Venezuela?

All in all, this is good. But then, the next question is: what about Saudi Arabia, Russia, Qatar, Venezuela, and number of other state-owned oil and gas companies tied closely to these countries GDP? How can we deal with those?

Here’s a list of the world’s biggest oil-producing countries of 2020.

As an example, the oil and gas sector is responsible for more than 60% of Russia’s exports and provide more than 30% of the country’s GDP.

Similarly, the sector accounts for roughly 87% of Saudi budget revenues, 90% of export earnings, and 42% of GDP.

In comparison, in the US the sector accounts for 7.6% of the countries’ GDP.

Run, hippo, run!

The energy transition is – as has been pointed out many times before – a crucial element in the transition to a sustainable future. The shift away from fossil dependency is modus operandi for both activists, investors and politicians (who are hoping to quell public expectations for action), and it does look better and better, at least if you read news and follow statements and articles.

The core issue is related to shifting not emissions, but entire business model of these integrated oil and gas companies that still, like it or not, support the energy infrastructure we use every day. Yes, every day.

It is not only transportation and energy, it is plastics, cosmetics and many other products we consume every day that depend on or are supported by fossil fuels.

So what is it we are asking of the oil and gas companies? In my opinion, it’s like asking a 2 tonnes heavy hippopotamus to run a 100 meter sprint in less than 10 seconds. Yeah, it sounds hard and rather comical. Not in relation to the hippo. More in relation to task at hand.

Why? Well, with the 2019 global GDP estimated to be $86 trillion, the oil and gas sector alone makes up around 3.8% of the global economy. Emerging economies have driven recent demand for the production of oil and gas. This is particularly true in the extremely populous BRIC nations: Brazil, Russia, India, and China.

So how do we talk to these countries about it? Some of the largest oil and gas companies in the world are NOT listed. Here are the 15 largest oil companies, and here’s where the oil reserves are located.

It’s hard to see activists let alone investors talk to the governments of 9 out of 10 countries on this list. And these are countries who are seeking to boost their GDP and in may cases feed their population.

How do we fix this? Yes, recent victories on some western listed companies are good progress, but the systemic issue goes deeper and is far more complex. We must not fool ourselves: the road to the light at the end of the tunnel will be very bumpy.

Are we ready for a just transition?

All of this relates to the topic of ‘just transition’. We need the transition to be just, otherwise it won’t happen. We need it to be just not only for ‘their’ sake, also for ‘our’ sake.

In other words: The transition needs to be managed very carefully. This includes:

We need to support the affected regions, sectors and industries with investments, knowledge and dialogue

We need to support workers, their families and the wider community affected by closures or downscaling

We need to address existing economic and social inequalities associated with the transition – it needs to be clear what it means

We need to ensure an inclusive and transparent planning process where the people and communities affected are involved and consulted.

The absolute impact of oil companies

One thing is all the words and all the statements, another is the feasibility of the change we all want and expect to happen. Some will say that it’s all about expectation management. Others will say it is not only doable, but both the right and the smart thing to do.

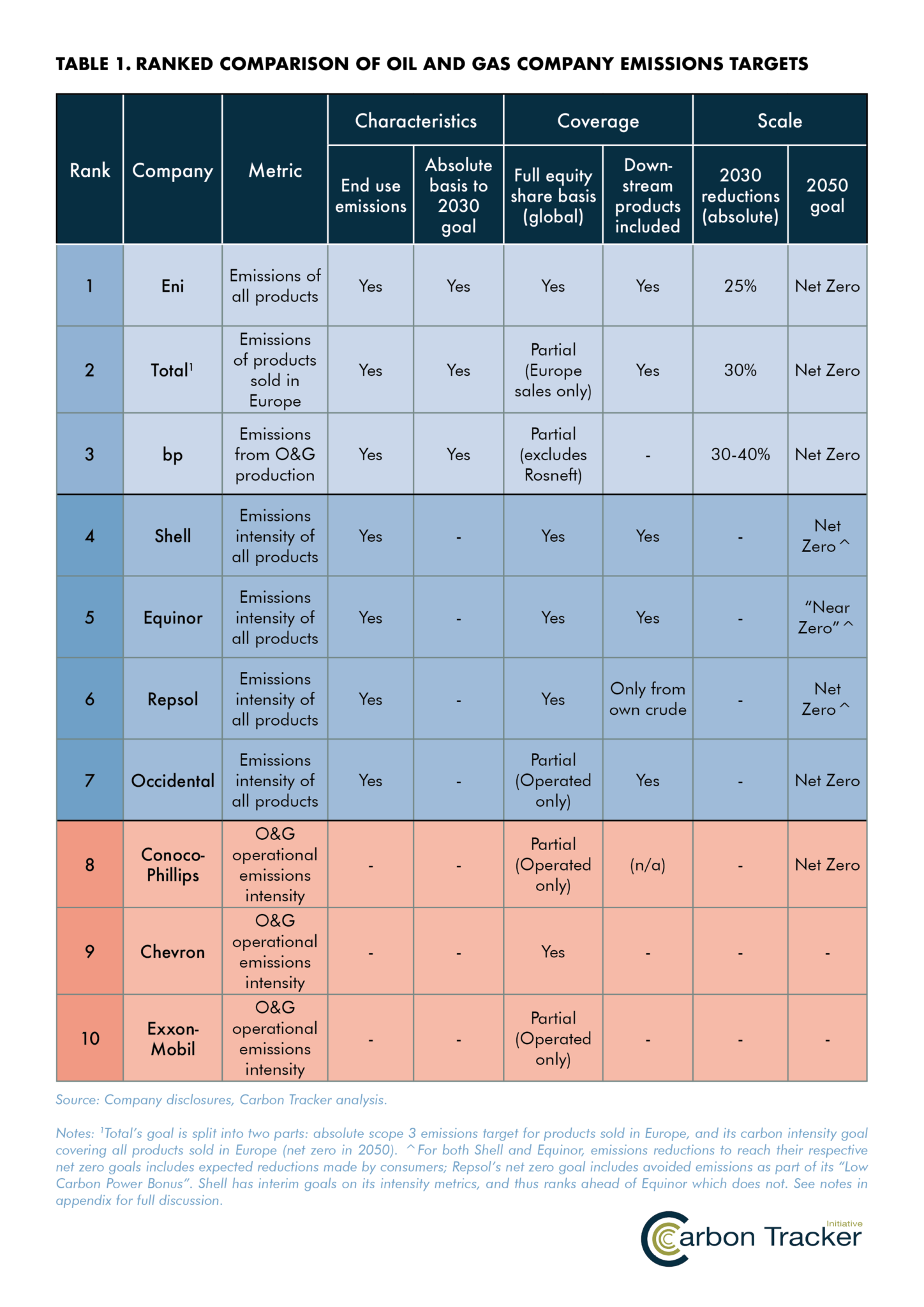

One of the questions lurking in the shadows of the “net-zero” commitments is how these companies will do what they are expected to do. Let’s have a look at how hard this could be for number of oil and gas companies.

Carbon Tracker has produced an absolute impact report on a number of oil and gas companies. Absolute impact is a bit, or rather a lot, different from other type of impacts.

The key here is that corporate climate goals in the oil and gas industry must link to finite limits that the energy transition places on current business models – and that’s not happening at the moment.

The findings are very, let’s just say ‘interesting’, and so is the ranking:

How oil and gas executives – as well as the larger global investment community – view this is another thing. You can find a useful article and analysis here.

From what to how

So, hopefully, we are no longer in the space of discussing the what, i.e. that we need to cut emissions in the oil and gas sector, but now in the space of the how. That doesn’t make it less complex or difficult.

How to best get there will depend on many, many different factors. The specific initiatives a company chooses to reduce its emissions will depend on factors such as its geography, asset mix (offshore versus onshore, gas versus oil, upstream versus downstream), and the local policies and practices (regulations, carbon pricing, the availability of renewables, and the central grid’s reliability and proximity).

In this report you can find an insightful description of how oil and gas companies can decarbonise.

From energy to finance

Moving on from energy to finance is usually a very short walk. The two areas are interconnected and interdependent in so many ways. What are the realities of the environmental risk factors, the real outcomes of decisions and lack of decisions in this space?

In a report entitled “The Anthropocene reality of financial risk” you can – and I suggest you do – read about the real consequences created by financial decision or lack thereof.

This is probably why, when someone in the financial sector sells you “impact” or claims “SDG impact”, you should think very carefully about it. Estimating potential positive impact is one thing, claiming impact as de facto is a bogus business.

There’s a blindspot in ESG investing

Small is beautiful, especially in the circular and sustainable world to come. This is – or should – also be the case with regards to ESG, because ESG is in many ways better suited to small and medium sized companies since their lead time to change and improve things is much shorter.

Unfortunately, there is a huge blind spot in the ESG investment market. Smaller companies are consistently being overlooked by investors with an ESG mandate. Corporate and public pensions, endowments, and foundations invest the majority of assets earmarked for ESG into the largest public companies.

In part, that’s because true ESG initiatives don’t come cheap and big public companies have used their deep pockets to adopt expensive reporting, standards, and disclosure programs, whether or not those policies ultimately lead to better ESG outcomes.

At the same time, they’ve also been able to define some ESG best practices, such as the optimal structure of a board – even when those practices may not make sense for smaller companies.

The positive side of the disparity between large and small companies is that small-cap stocks are relatively unploughed territory for investors looking to invest through an ESG lens or use ESG information for risk management.

You can read more on this here.

World’s biggest insurers fail to tackle ESG risks

How insured (safe, protected, comfortable) are you? How does your insurance company really protect you and your future (when they invest your insurance payments all around the world in different financial products)?

Well, it’s challenging. According to this analysis from ShareAction the world's biggest insurers are failing to tackle ESG risks. The analysis – which ranks the world’s 70 largest insurance firms – has found that none of them exclude companies driving biodiversity loss and just 13% exclude firms knowingly in breach of human and labour rights requirements.

The analysis assigns each of the companies a grade from 'AAA' to 'E' on the climate change impacts, biodiversity impacts, human rights implications and governance structures of their portfolios. And across all topics, almost half (47%) of the firms received an average of an ‘E’ grade – the lowest possible.

Performance, generally, was found to be weaker from firms in the US and Asia than those in Europe – a trend ShareAction attributes to “strong policy signals from the EU”, such as the introduction of the Sustainable Finance Disclosures Regulation (SFDR).

However, all assessed companies received a bottom grade (‘D’ or ‘E’) in at least one area.

The green bond scams continue

Do you remember we talked about green bonds? Well, some of the scams in this space are still happening.

The latest one is this: a South Korean electric utility issued green bonds last year while investing in new coal-fired power plants in Southeast Asia.

Watch my TV show… 📺

If you want even more of me (I completely understand if this newsletter is more than enough 😀), then you can tune in to the ESG series “Sustainability with Sasja” on Direkt Studios, every second Monday.

Here’s the link to the channel on YouTube:

That would be all for now. Have a great week!

Best regards,

Sasja